What is Accrual in Finance?

Have you ever heard the term accrual in a finance-related conversation and wondered what it means? Accruals play a significant role in accounting and finance, but they can seem confusing at first. Don’t worry, though—let's break it down together!

CAPITAL MARKETBLOGFEATURED

Understanding Accruals: The Basics

Accrual, in finance, refers to the process of recognizing revenue and expenses when they are earned or incurred, rather than when the money is actually received or paid. This method, known as accrual accounting, gives a more accurate picture of a company’s financial position over time because it matches income and expenses to the period in which they are earned or incurred.

Example:

Imagine you run a small business. You provided services in December, but you won’t receive payment until January. In accrual accounting, you would record the revenue in December when the service was performed, not in January when the payment is received. Similarly, if you receive a bill for services in December but pay it in January, the expense would still be recorded in December.

Why is Accrual Important?

Accruals are important because they allow businesses to track financial performance more effectively. By recording revenue and expenses when they are earned or incurred, businesses get a more accurate view of their financial health, allowing better decision-making.

If businesses used only cash accounting, they would record revenue and expenses when cash changes hands. While simpler, this approach could give an incomplete picture, especially for businesses with long-term projects or those offering credit.

Types of Accruals

There are two primary types of accruals in finance:

Accrued Revenue: This is revenue that has been earned but not yet received in cash.

Accrued Expenses: These are expenses that have been incurred but not yet paid.

Accrued Revenue: Example and Explanation

Accrued revenue is revenue that has been earned but for which the payment hasn’t been received yet. This commonly occurs in businesses where customers are billed at the end of a service period or after a project is completed.

Formula:

Accrued Revenue = Revenue Earned – Payments Received

Example:

Let’s say you own a consulting firm, and you completed a project worth ₹50,000 in December, but the client will pay in January. Under the accrual method, the ₹50,000 is recorded as revenue in December when the service was completed, even though you won’t receive the cash until January.

Accrued Expenses: Example and Explanation

Accrued expenses are costs that a business has incurred but hasn’t yet paid. These expenses are recognized in the period when they occur, not when the actual payment is made.

Formula:

Accrued Expenses = Expenses Incurred – Payments Made

Example:

Suppose your business rents office space, and rent for December is ₹20,000, which you will pay in January. Under accrual accounting, the ₹20,000 is recorded as an expense in December because that’s when the cost was incurred, even though the payment is made in January.

Accruals Across Different Asset Classes

Now that we understand the basics, let’s look at how accruals work across different asset classes.

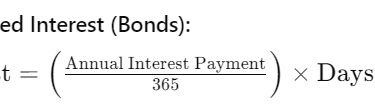

1. Bonds and Fixed Income

In fixed income, particularly with bonds, interest is earned over time, and this interest accrues as part of the bondholder’s earnings. Interest income is often earned daily but may be paid semi-annually. This accrued interest is recognized before the actual cash payment.

Example: If a bond pays 5% interest annually but payments are made every six months, you would accrue the interest over time rather than waiting until the end of the period to recognize the full amount.

2. Equities

While stocks (equities) don’t accrue interest, dividends declared but not yet paid can be considered an accrued revenue for investors. Once the company declares a dividend, it becomes an asset (even if it hasn’t been paid yet).

Example: Suppose a company declares a dividend of ₹10 per share on December 15, but it won’t be paid until January. Shareholders would accrue the ₹10 per share as revenue in December.

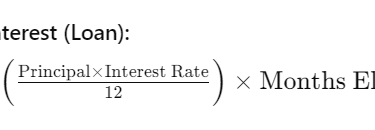

3. Loans

In the case of loans, both lenders and borrowers use accrual accounting. For the lender, the interest on the loan accrues over time, even though they may receive the payment in installments or after a set period. For borrowers, the expense accrues similarly, even though they might not pay it immediately.

Example (Lender): A bank lends ₹1,00,000 to a borrower at 12% annual interest, and the loan term is one year. If the loan was disbursed in June, by the end of December, 6 months of interest has accrued, even if the payment is due at the end of the loan term.

4. Real Estate

In real estate, rental income can accrue even if the cash has not been received. If a tenant occupies a property in December but doesn’t pay rent until January, the landlord accrues the rental income in December.

Example (Rental Income):

A landlord leases a property for ₹30,000 per month. If the tenant occupies the property in December but pays the rent in January, the ₹30,000 is still recorded as revenue for December.

Benefits of Using Accruals

Accruals provide several advantages to businesses and investors alike. Here’s why they are so important:

More Accurate Financial Statements: Accruals allow businesses to match revenue and expenses to the correct periods, making financial statements more reliable.

Helps in Planning and Budgeting: Since expenses and revenues are recognized when they occur, businesses can better anticipate future cash flows and plan accordingly.

Reflects Economic Reality: Accrual accounting shows the true economic activity of a business, regardless of when cash transactions happen.

FinCapKnowledge © 2024

FinCapknowledge empowers the generation of tomorrow for a brighter future and hope for every individual know is keen to learn finance.

FOR LATEST UPDATE

Subscribe to our newsletter and never miss a story.

We care about your data in our privacy policy.